Written by: Bootly

After five years of operation, raising approximately $180 million in total funding, and reaching a valuation once nearing $1 billion, Farcaster has officially admitted: the path of Web3 social has not succeeded.

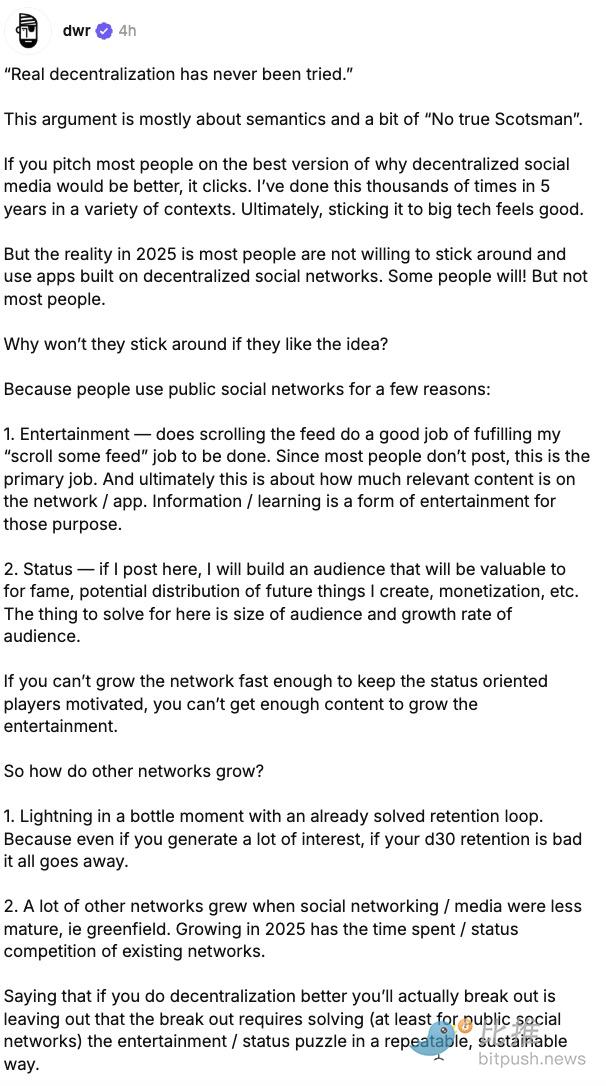

Recently, Farcaster co-founder Dan Romero posted a series of messages on the platform, announcing that the team will abandon the "social-first" product strategy and instead fully focus on the wallet direction. In his words, this is not an active upgrade but a choice forced by reality after a long period of attempts.

"We tried social-first for 4.5 years, and it didn't work."

This judgment not only signifies Farcaster's transformation but also once again highlights the structural challenges of Web3 social.

The Gap Between Ideal and Reality: Why Farcaster Failed to Become the 'Decentralized Twitter'

Farcaster was born in 2020, during the rise of the Web3 narrative. It attempted to solve three core problems of Web2 social platforms:

-

Platform monopoly and censorship

-

User data not belonging to users themselves

-

Creators unable to monetize directly

Its design approach was highly idealistic:

-

Decentralized protocol layer

-

Freedom to build clients

-

Social relationships on-chain and migratable

Among the various "decentralized social" projects, Farcaster was once considered the product closest to PMF. Especially after Warpcast gained traction in 2023, many KOLs from Crypto Twitter joined, making it seem like the prototype of the next-generation social network.

But problems soon emerged.

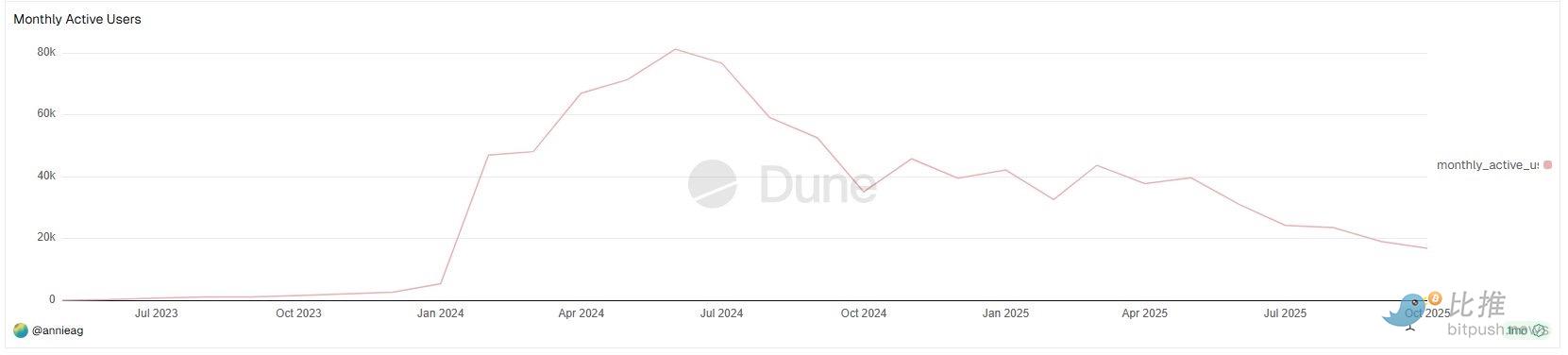

According to Farcaster's monthly active user (MAU) statistics on Dune Analytics, Farcaster's user growth trajectory shows a very clear but not optimistic pattern:

For most of 2023, Farcaster's monthly active users were almost negligible;

The real growth inflection point occurred in early 2024, with MAU rapidly increasing from a few thousand to about 40,000–50,000 in a short time, and even approaching 80,000 by mid-2024.

This was Farcaster's only truly scalable growth window since its inception. It is particularly noteworthy that this growth did not occur during a bear market but during a period of high activity in the Base ecosystem and the emergence of dense SocialFi narratives.

However, this window did not last long.

Starting in the second half of 2024, monthly active data showed a clear decline, and over the following year, it exhibited a volatile downward trend:

-

MAU rebounded multiple times, but the peaks continued to lower

-

By the second half of 2025, monthly active users had fallen to less than 20,000

In fact, Farcaster's growth has always been unable to "break through," with its user structure highly homogeneous:

-

Crypto practitioners

-

VCs

-

Builders

-

Crypto-native users

For ordinary users:

-

High registration barrier

-

Social content is heavily "insider-focused"

-

User experience not better than X / Instagram

This prevented Farcaster from ever forming true network effects.

DeFi KOL Ignas (@DeFiIgnas) on X bluntly stated that Farcaster "just admitted what everyone has felt for a long time":

The strength of X's (formerly Twitter) network effects is almost impossible to break head-on.

This is not a problem with the crypto narrative but a structural barrier of social products. From a product perspective, the issues with Farcaster's social side are very typical:

-

User growth has always been locked into the crypto-native crowd

-

Content is highly insular and difficult to spill over

-

Creator monetization and user retention did not form a positive feedback loop

This is why Ignas succinctly summarized Farcaster's new strategy in one sentence:

"It's easier to add social to a wallet than to add a wallet to a social product."

This judgment essentially admits that "social is not the first-order need of Web3."

"The Bubble Is Comfortable, but the Numbers Are Cold"

If MAU data answers "how Farcaster performed," then another question is: How big is this market itself?

Crypto creator Wiimee provided a set of striking comparative data on X.

After "accidentally stepping out of the crypto content circle," Wiimee created content for a general audience for four consecutive days. His analysis data showed that in about 100 hours, he received 2.7 million impressions, more than double the total views of all his crypto content over a year.

He stated:

"Crypto Twitter is a bubble, and it's small. Four years of speaking to insiders is less effective than four days of speaking to the masses."

This is not a direct criticism of Farcaster but reveals a more fundamental problem:

Crypto social itself is a highly self-referential ecosystem with weak spillover capabilities. When content, relationships, and attention are all confined to the same batch of users, even the most refined protocol design cannot break through the upper limit of market scale.

This means Farcaster faced not "the product isn't good enough" but "there aren't enough people in the field."

Wallet, on the Other Hand, Achieved PMF

What truly changed Farcaster's internal judgment was not a reflection on social but the unexpected validation of the wallet.

Earlier in 2024, Farcaster introduced a built-in wallet in its application, initially intended only as a supplement to the social experience. But from usage data, the wallet's growth slope, frequency of use, and retention performance were significantly different from the social module.

Dan Romero emphasized in a public response:

"Every new and retained wallet user is a new user for the protocol."

This statement itself reveals the logical core of the strategic shift. The wallet addresses not "the desire to express" but real, rigid on-chain behavioral needs: transfers, transactions, signatures, and interactions with new applications.

In October, Farcaster acquired Clanker, an AI Agent-driven token issuance tool, and gradually integrated it into the wallet system. This move was also seen as the team's clear bet on the "wallet-first" path.

From a business perspective, this direction has clear advantages:

-

Higher frequency of use

-

Clearer monetization path

-

Tighter integration with the on-chain ecosystem

In contrast, social seems more like a nice-to-have rather than an engine for growth.

Although the wallet strategy is justified by the data, community controversy has also followed.

Several long-term users explicitly stated that they are not opposed to the wallet itself but are uncomfortable with the cultural shift that comes with it: from "users" being redefined as "traders," from "co-builders" being labeled as "old guard."

This exposes a practical problem: when a product direction changes, community sentiment is often harder to migrate than the roadmap. Farcaster's protocol layer remains decentralized, but the choice of product direction is still concentrated in the hands of the team. This tension is amplified during transformation.

Romero later admitted that there were communication issues but made it clear that the team had made its choice.

This is not arrogance but a common decisive reality for startup projects in the later stages of their lifecycle. In this sense, Farcaster did not abandon the social ideal but gave up the illusion of its scalability.

As one observer perhaps put it best:

"First, let users stay for the tools; then there is space for social to exist."

Farcaster's choice may not be the most romantic, but it might be the one closest to reality. Deeply integrating native financial tools (wallets, transactions, issuance) is the practical path to converting into sustainable commercial value.